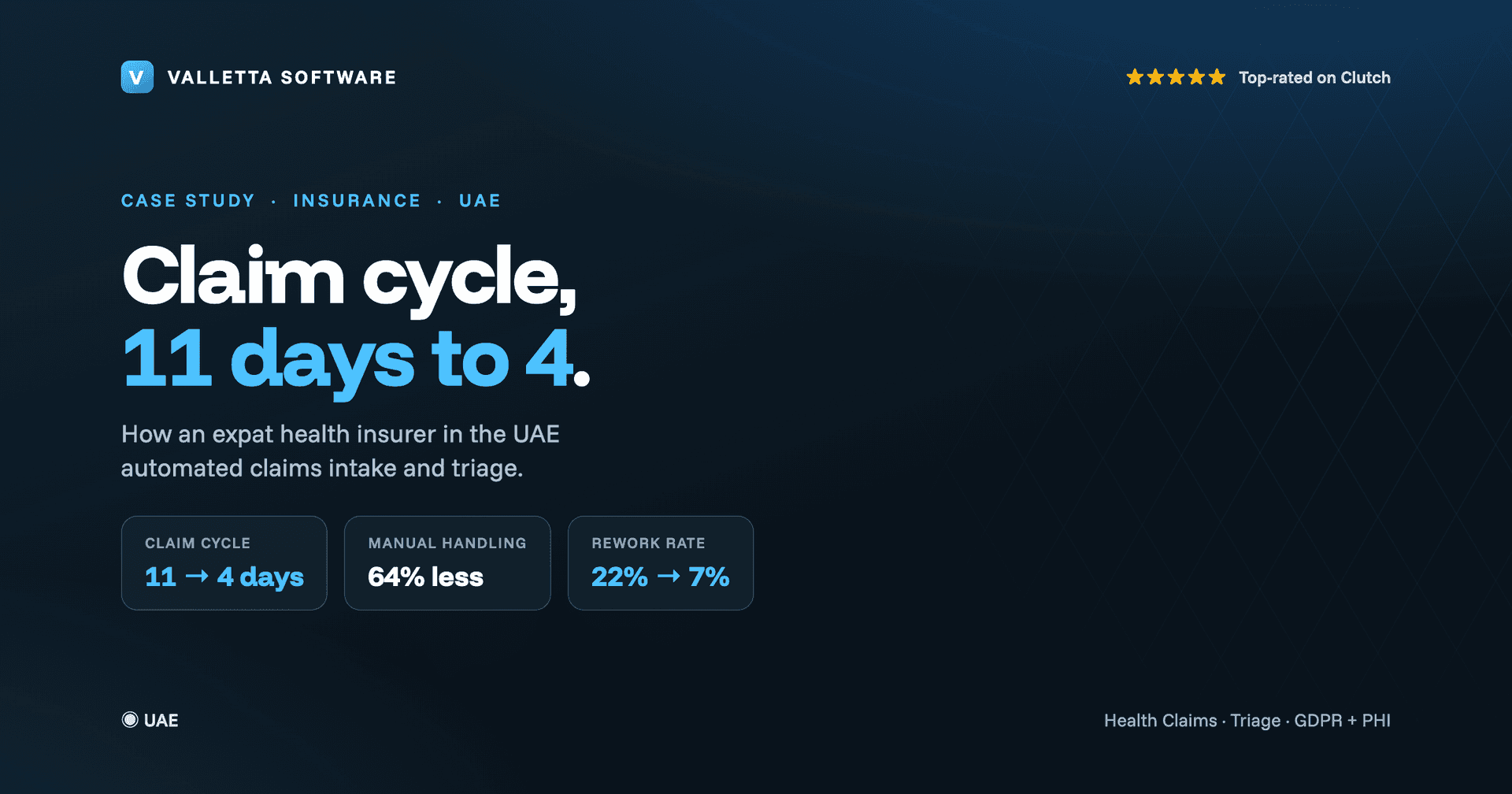

How an Expat Health Insurer in the UAE Cut Claim Cycle Time From 11 Days to 4

An expat health insurer in the UAE was processing around 9,000 claims a month by hand, with each claim touched by three people and a cycle that averaged 11 days. After a five-day Discovery audit and a focused build, simple claims now flow straight through and the average cycle has fallen to four days.

Key Takeaways

- Average claim cycle fell from 11 days to 4 (about 2.75x faster)

- Manual claim handling dropped 64%

- Rework from missing information fell from 22% to 7%

- Cost per claim processed fell 38%, with senior adjusters freed for complex cases

The client is an expat-focused health insurer in the UAE, with a claims team of around 50 people handling roughly 9,000 claims a month for internationally mobile members. For confidentiality we describe the engagement without naming the firm or the people involved.

The Challenge: Internationally Mobile Members, a Manual Claims Queue

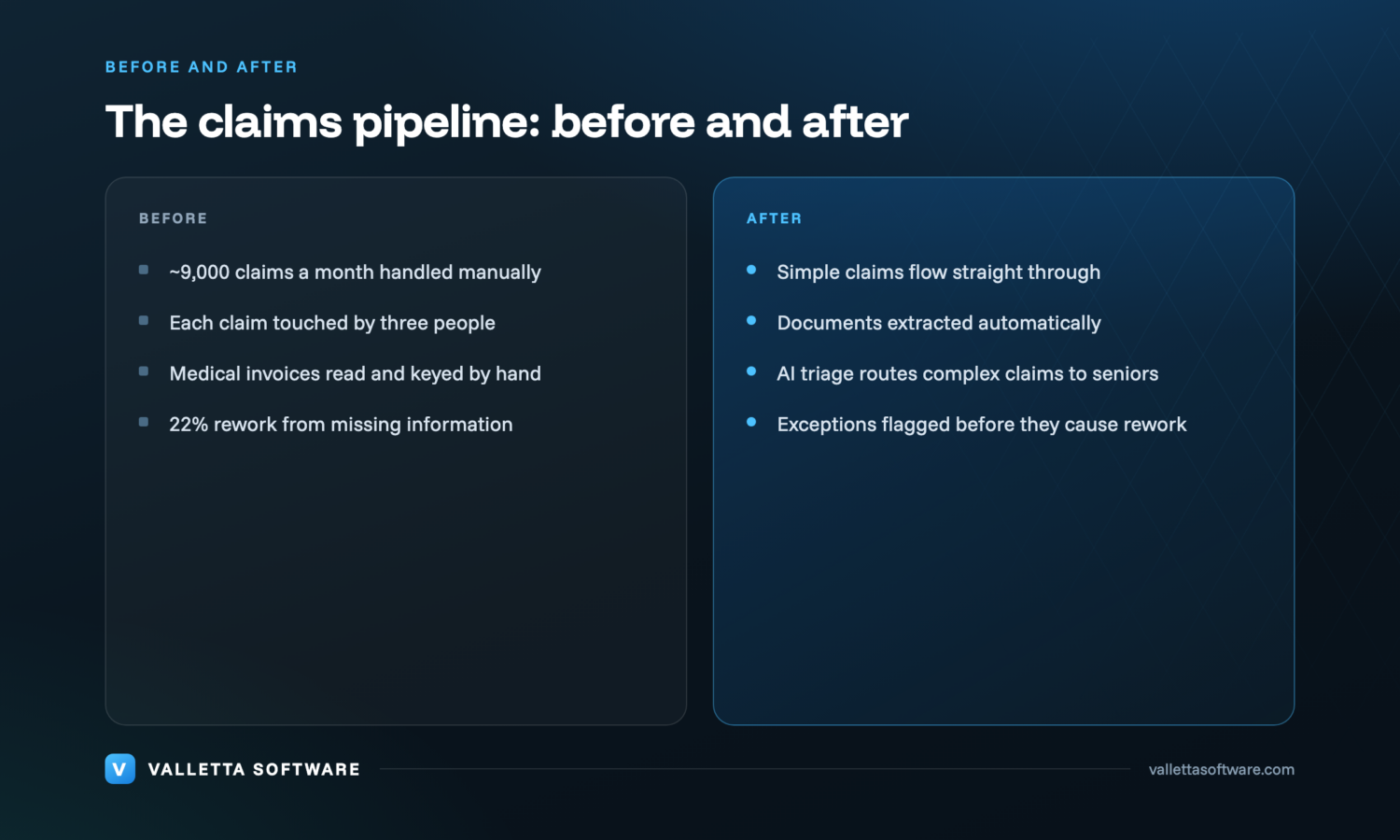

The insurer's members live and work across borders, and they file claims in the middle of a relocation, a business trip, or a family health crisis. An 11-day average cycle was not a minor inconvenience for those members; it was a tangible failure at precisely the moment coverage was supposed to matter. The claims team of around 50 people was processing roughly 9,000 claims a month, and almost every one of them passed through three sets of hands before a payment decision was made.

The rework problem compounded the speed problem. Around 22% of claims had to be reopened because supporting information, a missing invoice line, an incomplete diagnosis code, or an illegible receipt, was only discovered after the claim had already moved along the queue. Each rework cycle added days, consumed adjuster time, and frustrated members who had already waited. Senior adjusters spent much of their week on simple cases that had stalled, rather than on the complex ones that genuinely needed their judgment.

A five-day Discovery audit put concrete numbers to what the team already felt:

- ~9,000 claims a month handled manually

- Each claim touched by three people

- Medical invoices read and keyed by hand

- 22% rework from missing information

The Approach: A Five-Day Discovery Audit

We started with a five-day Discovery audit rather than a technology proposal. Two of our engineers embedded with the claims team for a full working week, following live claims from first notification through to payment decision, timing every handoff, and interviewing adjusters at each stage of the queue.

The audit produced three findings that shaped everything that followed. First, roughly two thirds of claims were straightforward, low-risk cases that still moved through three people simply because the workflow had no mechanism to distinguish them from complex ones. Second, document extraction was the single slowest manual step, and the illegibility or incompleteness of medical invoices was the source of almost all the rework. Third, the insurer's member population included EU nationals, meaning that protected health information had to be handled under a rigorous compliance framework from the first day of design. The non-negotiable constraint was this: no member health data could be processed outside a controlled, auditable environment. That ruled out public AI services entirely, and it anchored the architecture around a private deployment with explicit data-residency controls. All of this had to satisfy the EU General Data Protection Regulation as the applicable standard for members whose home jurisdiction sits within the EU.

With those findings in hand, we had a clear brief: separate the simple from the complex, fix extraction before triage, and build compliance into the pipeline structure rather than layering it on after the fact.

The Solution: Straight-Through Processing for Simple Claims, AI Triage for the Rest

We built a claims pipeline that routes work to the right place the first time: simple, rule-bounded cases proceed automatically, and complex or high-value cases go directly to a senior adjuster with the relevant context already assembled. The pipeline is structured around four stages, each designed to eliminate a specific source of delay or rework.

- Intake. First notifications and supporting documents are captured automatically from email and upload channels, with each claim opened, timestamped, and indexed without any manual keying. This eliminates the delay between a member submitting a claim and a file existing in the system, which was previously measured in hours during busy periods.

- Extract. Medical invoices, receipts, and supporting clinical documents are read and structured automatically, with field-level confidence scoring applied to every extraction. Any field that falls below the confidence threshold is flagged for human review before the claim advances, stopping the missing-information rework cycle at its source rather than discovering the gap two days later.

- Triage. Each claim is scored against a set of explicit business rules covering value, complexity, diagnosis category, and policy type, and then routed accordingly: simple, low-risk claims within the defined rules proceed straight through, while anything ambiguous, high-value, or outside the rule set goes directly to a senior adjuster. The routing logic is fully auditable and the rules are maintained by the insurer's operations team, not embedded invisibly in the model.

- Adjudicate. Adjusters work from an exception queue rather than a full claims queue, with the system pre-filling each file with the extracted data, the triage rationale, and the relevant policy context. This means adjudicators spend their time making decisions rather than assembling information, and every decision is documented with a clear, searchable record.

Health claims data is among the most sensitive personal data processed in any industry. Protected health information carries legal obligations under multiple frameworks, and a failure in security or data handling is not just a compliance risk but a direct harm to members. Security and compliance were the first design requirements on this project, not a checklist added at the end:

- Protected health information is encrypted in transit and at rest using current standards, with strict role-based access controls ensuring that each adjuster and team member can view only the claims within their authorized scope, and with full audit logging of every view, extraction, edit, and decision so that any access to member health data is permanently and specifically recorded.

- The pipeline operates in full compliance with the EU General Data Protection Regulation for the insurer's EU-national members, including documented lawful basis for processing, data minimization applied at each pipeline stage, and a data processing agreement that the insurer can present to regulators or member representatives on request.

- All processing runs within a private, single-tenant deployment with explicit data-residency controls, keeping member health data within defined geographic boundaries and fully isolated from shared infrastructure; no member data is ever sent to public AI services, shared AI training pipelines, or any third-party model provider.

- Access to the system is governed by least-privilege role assignments, and straight-through processing is bounded by explicit, insurer-defined rules so that any claim with ambiguity, elevated value, or an unusual presentation always routes to a qualified human adjudicator who retains the final decision authority.

Members move between countries and expect their claim to keep up. Eleven days was not keeping up.

The design kept the human adjudicator accountable for every claim that warranted judgment. Straight-through processing applied only where the rules were unambiguous and the risk was low, and the team could see exactly which claims had been processed automatically and on what basis.

The Results: Faster Claims, Less Rework, Adjusters on the Hard Cases

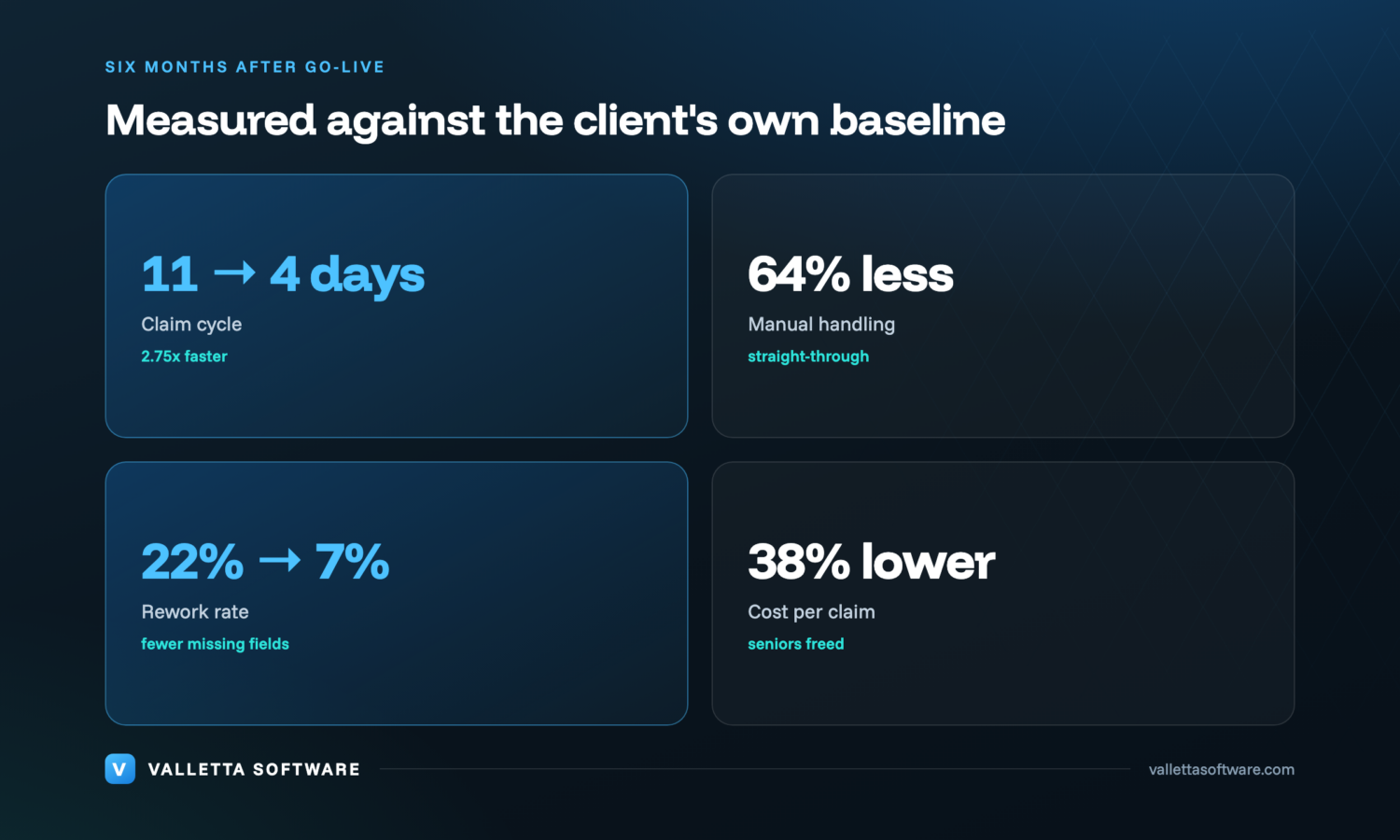

We piloted the pipeline on a single claim type with a well-defined rule set, ran it in parallel with the existing process for four weeks to validate accuracy and straight-through rate, then widened the scope incrementally across claim types. Six months after full go-live, the operation had changed measurably across every metric the insurer tracked.

- Average claim cycle fell from 11 days to 4 (about 2.75x faster).

- Manual claim handling dropped 64%.

- Rework from missing information fell from 22% to 7%.

- Cost per claim processed fell 38%, with senior adjusters freed for complex cases.

The insurer's most experienced adjusters spent their time on the cases that needed them, members received decisions in days rather than approaching two weeks, and the rework cycle that had quietly consumed a fifth of all claims was reduced to a small, manageable exception rate. The cost to process each claim fell 38%, not by reducing headcount but by redirecting the same team's capacity toward higher-value work. To see how we approach automation projects across the insurance sector, visit our insurance automation services.

Frequently Asked Questions

Is it safe to automate health claims given how sensitive medical data is?

Yes, when it is designed for it. Protected health information is encrypted, access is strictly role-based, processing runs in a private deployment with data residency controls, and no member data is ever sent to public AI services.

Does automation mean claims get approved without a human?

No. Straight-through processing applies only to simple, low-risk claims within set rules. Anything ambiguous or high-value is routed to a qualified adjuster, who keeps the final decision.

Start With a Five-Day Discovery Audit

If your claims team is touching every claim by hand, regardless of complexity, the simple cases are quietly consuming the capacity your senior adjusters need for the hard ones. The fastest way to understand how much that is costing, and which claim types are safe candidates for straight-through processing, is a five-day Discovery audit. We map the real workflow, measure the actual rework sources, and produce a costed, prioritized plan that accounts for your compliance obligations from the first page.

In five working days, for a fixed fee of €2,000, two of our engineers map your real workflow, measure where the manual hours and errors actually sit, and hand you a costed, prioritized automation plan, whether or not you build it with us.

Book your five-day Discovery audit: vallettasoftware.com/malta-ai-automation/insurance